If past mortgage activity is a barometer, the Riverside-San Bernardino, CA, metro area could be hit especially hard by the Trump administration’s decision to halt a planned cut in FHA mortgage insurance premiums.

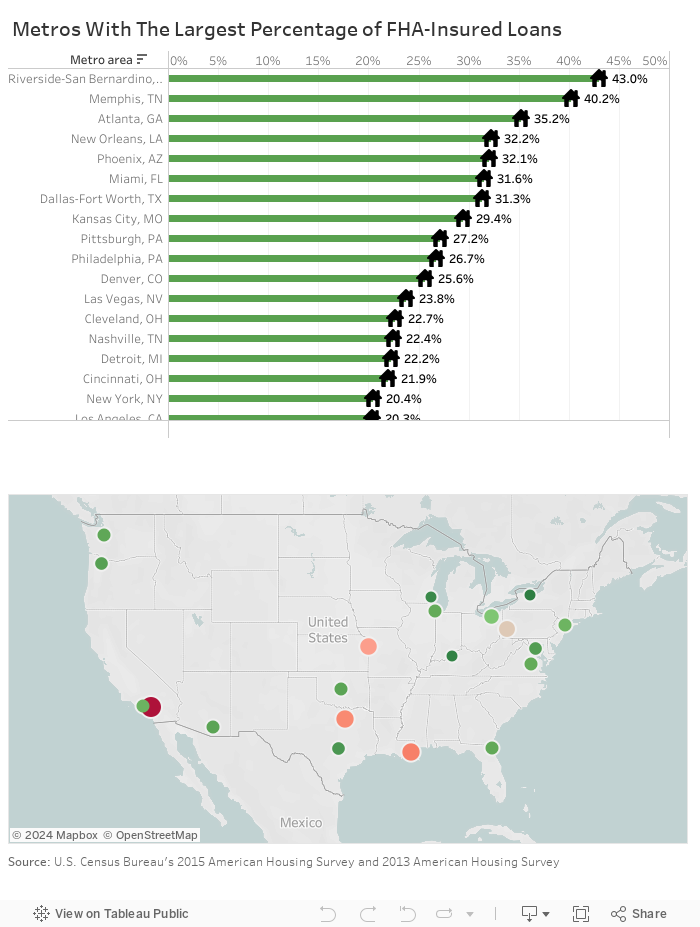

A LawnStarter review of data from the U.S. Census Bureau’s American Housing Survey shows that in 2015, nearly 43 percent of home mortgages in the Riverside-San Bernardino area were insured by the Federal Housing Administration (FHA). That was the highest share of FHA-backed mortgages among 40 major metro areas included in the American Housing Survey in either 2013 or 2015; we analyzed the most recent data for each metro.

Four of every 10 homebuyers in Riverside-San Bernardino, CA, rely on FHA loans.

Photo: Redfin

The California Association of Realtors says the FHA premium rollback would have saved homebuyers in Riverside-San Bernardino and throughout the state an average of $860 a year. California “will be negatively impacted more than any other state by the decision to not reduce the FHA premium,” the association says.

The California association has called on the Trump administration to review the “merits” of the premium reduction and immediately lift the suspension.

Based on our analysis, here are five major metro areas that could be harmed the most by the FHA action.

1. Riverside-San Bernardino, CA

Share of FHA-backed mortgages: 42.99%

2. Memphis, TN

Share of FHA-backed mortgages: 40.21%

3. Atlanta, GA

Share of FHA-backed mortgages: 35.19%

4. New Orleans, LA

Share of FHA-backed mortgages: 32.24%

5. Phoenix, AZ

Share of FHA-backed mortgages: 32.05%

At the end of this blog post is a complete list of metro areas ranked by their dependence on FHA-backed mortgages.

Realtors ‘Disappointed’ by Decision

While mortgage data from two or four years ago cannot predict how a metro like Riverside-San Bernardino will fare under the FHA change, it does offer an indication of how homebuyers there and in other major metro areas could be affected by the Trump administration’s move.

William Brown (left) is president of the National Association of Realtors.

Photo: PRNewsFoto/National Association of Realtors

On Jan. 9, the FHA, under the Obama administration, had announced a reduction in annual premiums from mortgage insurance from 0.85 percent of the outstanding loan balance to 0.60 percent. The cutback was supposed to take effect Jan. 27. However, on Jan. 20 — the day of President Trump’s inauguration — the FHA indefinitely suspended the premium decrease. In a letter announcing the decision, the FHA said it “is committed to ensuring its mortgage insurance programs [remain] viable and effective in the long term for all parties involved, especially our taxpayers.”

The National Association of Realtors (NAR) says the scheduled lowering of FHA insurance premiums would have trimmed $500 a year in expenses for the average FHA borrower. Now, the NAR says, the Trump administration’s reversal could stick an estimated 750,000 to 850,000 homebuyers with higher costs, and leave 30,000 to 40,000 would-be homebuyers out of the home market altogether.

“We’re disappointed in the decision,” NAR President William Brown, a Realtor from Northern California, says in a statement, “but will continue making the case to reinstate the cut in the months ahead.”

FHA Loans in the Inland Empire

As explained by the Los Angeles Times, the FHA does not issue home loans, but rather insures mortgages and collects fees from borrowers to reimburse lenders in case a homeowner goes into default. Across the country, the FHA guarantees about 18 percent of all mortgages for homebuyers.

Of course, in Riverside-San Bernardino — known as the Inland Empire — the percentage of FHA-backed mortgages is much greater than that. Why does the region rely so heavily on FHA-backed loans? Part of the answer lies in the generally poor credit history of its population.

In 2016, Experian, one of the three major credit-reporting bureaus, identified Riverside as being the U.S. city with the fourth-lowest credit score: 632. Nationally, Experian’s average credit score is 673. Homebuyers with low credit scores gravitate toward FHA-backed mortgages because of their credit-friendly terms.

Jeremy Colonna is a senior mortgage loan originator in Southern California.

Photo: Twitter/Jeremy Colonna

Jeremy Colonna, senior mortgage loan originator at Matchpoint Funding, a home lender in Southern California, says another reason for the high percentage of FHA-backed loans in Riverside-San Bernardino is the region’s relatively low income.

Median household income in the region was $56,087 in 2015, the Census Bureau says, compared with $64,500 for all of California. In Riverside-San Bernardino, 17.5 percent of residents had income below the federal poverty level in 2015, compared with 15.3 percent of all Californians.

An FHA-backed loan is attractive to lower-income households because a buyer with a higher-than-normal ratio of debt to income can more easily qualify for this type of mortgage than a conventional mortgage, Colonna says.

Joshua Summers is a Redfin real estate agent in the Riverside-San Bernardino area.

Photo: Redfin

On top of that, low income typically translates into lower savings rates, he says, meaning a potential buyer might not have enough money stashed away for a down payment on a conventional mortgage. However, FHA-backed loans require only a 3.5 percent down payment — less than most traditional mortgages.

Additionally, Colonna says, median home prices in Riverside-San Bernardino support a higher percentage of homes that are eligible for FHA-backed loans. Joshua Summers, a Redfin real estate agent who works in the Riverside-San Bernardino area, says someone can buy a three-bedroom home in the region for around $350,000 — less than half what you’d normally pay in nearby Los Angeles and Orange counties.

“We are seeing a healthy influx of buyers from the surrounding communities that are paying very high rents and realize they can have a lower mortgage payment and own a piece of property by moving to this area,” Summers says. “Many folks make pretty long commutes, but they consider it a fair tradeoff for the ability to build equity and own a piece of property.”

Top photo: City of Riverside